Powered by RedCircle

Why are my premiums going up so fast on my real estate insurance? The usual VCREP gang was off this week, but instead we have commercial real estate experts Rod MacKay and Seamus Bailey stepping into the studio to welcome Nigel Clark, Senior Vice-President – Construction and Commercial Real Estate of BFL Canada.

Working for one of the largest risk management, insurance brokerage and benefits consulting firms in Canada, Nigel knows the commercial real estate insurance industry inside and out. He talks about how inflation, interest rates, and rising construction costs all impact the insurance market, and dives into the difference between a soft-market and hard-market, as well as diagnosing the type of market we are currently in.

You might also be surprised to hear what direction the insurance market is going in and how this directly affects consumers. He unpacks the previously volatile strata insurance market, how a recession can influence insurance policies, and much more.

Who is Nigel Clark?

I am the Senior VP of Construction and Commercial Real Estate at BFL Canada. I’ve been with BFL Canada for over 12 years and our immediate team is about 50 people strong. I live in East Vancouver with my wife and two young daughters.

We were primarily a construction team when we first came together in 2004. But many of our construction clients retain their assets, so we’re able to manage both the construction and their operating assets.

How is inflation and increasing construction costs affecting insurance?

Insurance is no different than any other business in terms of exposure to inflation and rising costs. We’re not insulated from that; it’s prevalent in my day to day when I’m talking about insured values.

I just went through a large commercial real estate insurance renewal and the first thing we were asked to do is look at values. Clients need to ensure their values are up to date to reflect increased costs and inflation. But there’s no specific formula. We have to take a multi-prong approach to ensure both our clients and insurers are happy.

Just running an insurance company is expensive, so our insurers are looking to recoup their costs. That, in addition to inflation and rising construction costs, affects the cost of premiums.

How does the global market affect insurance costs?

Many insurers are multinational entities who insure assets around the world. So if there’s a wildfire in California or hurricane in Florida, that has ripple effects. Reinsurance costs bleed down into the costs that customers pay. Global disasters certainly have a broad effect.

For example, the flooding in the Fraser Valley last year and wildfires in the Okanagan and California have been a major factor for Vancouver real estate insurance. A lot of these properties are held by the same insurers who have to pay out the claims.

How has covid affected insurance policies?

Covid had a huge impact on the insurance industry. In the height of covid, insurers weren’t writing any new business or taking on any risks that weren’t profitable, like residential real estate. So covid compounded what was already a very difficult insurance industry. Covid exasperated issues that were already there.

Now, it has levelled off. There’s more appetite and capacity in the market; we have more flexibility for risk.

During covid, insurers met their obligations in their contracts but were very strict with what new business they would take on. Covid was new to us and it made the day to day of our business more difficult.

Communicable disease, like covid, is an exclusion on most policies. So it’s not like insurers were paying out a boatload of claims. It was just a general time of uncertainty when insurers decided to turn off the taps and wait to see what happens.

What is a soft market for insurance and what is a hard market? What type of insurance market are we in now in 2022 and where are we heading?

A soft insurance market has a lot of capacity – a lot of insurers are fighting for the same business. That reduces pricing and increases things like favourable deductibles, extensions and additional coverage.

Soft markets are nice for us as brokers because we can present more options to our clients at lower pricing. There’s more supply, so clients can be more flexible. It’s good news.

We were in a soft market for well over a decade prior to 2019. But the tide started to turn before covid.

A hard market for insurance is the opposite: there is finite capacity for the same level of demand which leads to increased rates, higher deductibles and reduced coverage. That is the market we are in now. It’s hard to have tough conversations with clients in a hard market and deliver that bad news.

In the last six months, we have seen more capacity creep in and that is starting to soften the market. It’s still a hard market, but it is softening.

Are there different insurance processes and policies based on asset class?

It doesn’t matter what asset class, insurance covers the same things. On the property side, you have protection against things such as theft, flood, earthquake, etc. And on the liability side, you have coverage against third party claims.

In terms of desirability, insurers prefer commercial and office risk over residential risk. There’s a higher propensity for claims with residential real estate. So the process is a bit easier under commercial, specifically office and retail, insurance policies.

There was a lot of news in the last couple of years about strata insurance policies skyrocketing. What happened and is it still happening?

There was a confluence of events that led to many strata insurance policies skyrocketing in 2019/2020.

The majority of strata insurance policies in BC are placed via 3-4 programs, with each program having 20-30 insurers under it. Each insurer has a share and takes a piece of the program.

In 2019/2020, a few insurers who had big shares in the program pulled out of the market. This was driven by losses. Our data showed that for every $1 strata insurers were collecting in premiums, they were paying out $4 in claims. And most of those claims were due to water damage. That can only go on so long before the insurers will demand changes.

Some insurers were paying out more than they were getting, so decided to pull out of these programs in North America all together. The insurers who were left said they needed higher rates and deductibles to make the numbers work. Covid then threw gas onto the problem. That’s how this all blew up and ended up in the news.

The strata insurance problem has plateaued and profitability in the space has come back a bit. Insurers are willing to play ball again. Deductibles are still high, especially for water damage, but that adjustment has allowed for more flexibility in this space.

With rising construction costs, do insurers find it more risky to insure developers for construction?

If you take a property policy out in the construction industry, that covers your project for physical damage from start to finish. Insurers are digging down more on the pro formas because these policies are based on estimated project values. If those values seem off, insurers may have questions.

But those value numbers are adjusted at the end of the term and clients will pay the difference if the numbers are off. So it’s not a huge risk for insurers because these construction policies are fluid.

We work with a lot of developers and package them up into the marketplace. If a developer or contractor has had a run of claims, it does come up. The insurers will want to have a conversation about that. But we can usually fix the issue by increasing deductibles or minimizing that person’s involvement.

Insurers look for frequency and severity of claims. If a builder has both of those things, that’s a red flag. But it usually results in tweaks to a policy, not in the insurer not writing at all.

How would a recession affect the insurance market?

If there’s a slowdown in the economy, that makes insurers hungry to continue growth. So that may actually improve our market. That’s my optimistic view. These companies all want to grow and will have to get more aggressive to do that during a recession.

If insurers are fighting for business, that’s good for us and good for our clients. But we will have to wait and see how things turn out.

Find out more: bflcanada.ca

Stephen Gammer, with over 15 years of experience in the Commercial Real Estate industry, shares his invaluable insights on what to expect during the commercial lease process, common pitfalls to avoid, and strategies to negotiate win-win situations for all parties involved.

Cameron Archer, Director of Sales and Marketing at Orion Construction, shares how they’ve managed to excel in a competitive market, from leveraging his background in managing industrial projects to nurturing client relationships. Also… listen in to learn how you can enter our Nickelback ticket draw!

Ben Vella, Chief Financial Officer of Rain City Industrial, delves into the intricate world of commercial real estate accounting. Ben sheds light on the crucial role of financial management in commercial real estate projects. From managing budgets to identifying cost savings opportunities for clients, Ben shares valuable insights on optimizing cash flow structures and maximizing tax savings.

Stathis Michael Savvis, Commercial Real Estate Broker at William Wright Commercial, unpacks the endless commercial real estate opportunities awaiting in Maple Ridge, accentuating its pro-business ethos and promising growth prospects within the Greater Vancouver area.

Nathan Armour, Team Lead at William Wright Commercial's New Westminster office, brings a wealth of expertise spanning property valuations, business sales, and investment opportunities. Gain insights into market trends, areas of activity, and the ever-evolving landscape of commercial real estate as Nathan unpacks his extensive knowledge.

With a vision to elevate the hospitality scene, William Donnellan, CEO and Founder of IRL Group, has been steering the expansion of Irish-inspired pubs throughout Vancouver. Gain insights into how IRL Group navigated the complexities of a post-pandemic market, adapting and expanding to meet the demands of a changing landscape.

David Basche, President of Astria Properties, provides unparalleled insights into the industrial asset class and its dynamic landscape. Delving into the nuances of industrial real estate, he also explores the evolving trends in the office asset class, including the topic of rezoning, particularly the shift from industrial to office sparked by recent industry trends.

Anita Chang, Partner with EY, discusses the intriguing intersection of entrepreneurship and real estate ventures. Anita shares EY's Entrepreneur Of The Year program, unveiling the significance and opportunities it presents for entrepreneurs in the real estate arena.

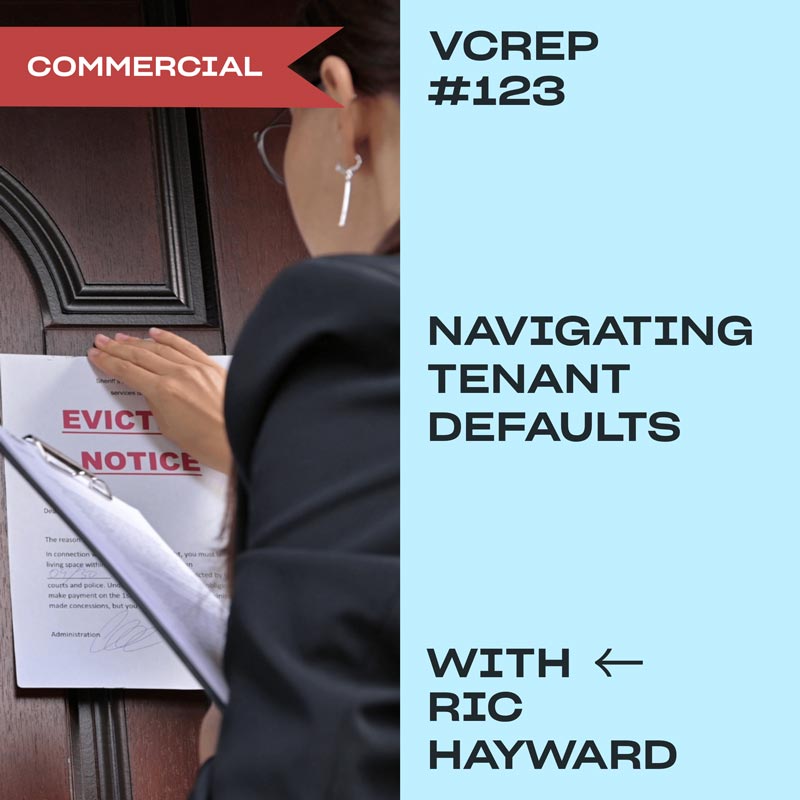

Ric Hayward of Lower Mainland Bailiff guides landlords through the intricate process of handling tenant defaults, offering indispensable insights into how bailiffs can serve as a valuable resource for both parties involved. Gain a comprehensive understanding how leveraging the expertise of a bailiff can be instrumental in resolving such situations.

Meg Cooney, seasoned Commercial Real Estate Broker from William Wright Commercial's Vancouver office, takes center stage to share insights into the world of pre-sale strategies in commercial real estate. This episode offers a valuable exploration of pre-sale tactics and market insights.

With his finger on the pulse of the real estate landscape, Alan Haigh of Impact Commercial provides a roadmap for the year ahead. Amidst market turbulence involving interest rates and inflation, Alan offers clarity on potential rate trajectories, strategies for seizing opportunities during market volatility, and insights to steer investors in the right direction.

In this concluding episode of the year, Matt and Cory offer a comprehensive summary of the year's journey through the dynamic world of commercial real estate. Together, they explore the transformative shifts within various asset classes, shedding light on how the commercial real estate landscape has evolved.

With an expert grip on international markets, Peter Leung, esteemed "Investorpreneur" and international correspondent, offers exclusive insights that can truly give investors a competitive edge. Explore his surprising viewpoints on the buy-sell dilemma and get ready to be astonished by his current pick for the ultimate investment hotspot.

Bob Knakal, a distinguished figure in New York City's commercial real estate scene, boasting an impressive 40-year tenure in the industry, delves deep into the intricate details of the NYC office market, the current vacancy rates, trends, and surprising lease rates for prime retail spaces.

Dan Smith, the driving force behind commercial leasing at Reliance Properties, takes center stage to delve into the pulse of the current commercial real estate market. Tune in to discover Dan's insights into the potential resurgence of the office asset class.

This week features an insightful conversation with Eric Wainwright, Managing Director of STOREYS. STOREYS covers and reports on the Toronto housing market. Being a leader in publishing digital content, Eric unpacks his thoughts on the current real estate market, from interest rates to challenges developers are facing and more.

It's time to reveal the top 5 commercial investment markets for 2024! Cory and Rod MacKay from WWC Vancouver break down the most promising opportunities for the year ahead. These markets offer above-average returns with significant potential for increased net operating income, paving the way for substantial equity gains.

As we step into the fall, anticipation builds for the unveiling of the Western Investor's top five cities to invest in for the year ahead. Frank O'Brien from the BIV Media Group, the editor behind the insightful Western Investor reports, presents the prime cities for commercial real estate in 2024.

Shelby Kostyshen, commercial real estate expert from the William Wright Commercial Kelowna office, sheds light on Vernon, a city that's recently seen an uptick in growth. Could Vernon be the next Kelowna? Shelby unpacks specific asset classes that mirror the trends unfolding in Kelowna.

Byron Chard, President and CEO of Chard Development, provides a comprehensive overview of the current state of the commercial real estate market. Byron sheds light on the recent GST changes affecting purpose-built rentals. What do these changes mean for investors and how are they impacting Chard Development's strategies?

As a hands-on expert, Jon Switzer of Impact Commercial shares invaluable insights into the commercial real estate landscape, offering listeners a comprehensive view of the present and a glimpse into the future. Tune in for an informative conversation that promises to shed light on the ever-evolving world of commercial real estate.

Back by popular demand, Douglas Porter, Chief Economist and Managing Director of Economics at BMO Financial Group, provides unparalleled insights into the current landscape of interest rates and offers a crystal-clear view of what lies ahead. Will the trend continue its upward trajectory or are we on the brink of a shift?

Heidi Shortreed from Vedderbrook Properties unveils the secrets to unlocking hidden profitability within your real estate ventures through the strategic use of property management. Tune in as Heidi shares her invaluable insights on how a seasoned property manager can be the key to turning your building into a revenue-generating powerhouse.

Jeff Hancock, who specializes in land development at the WWC Kelowna office, discusses the effects the recent forest fires have on the local market. These annual occurrences have become a part of life for this vibrant Okanagan city that has become a bubble for real estate development over the past few years.

Santanna Portman, Commercial Sales and Leasing Specialist at William Wright Commercial, dives into the vibrant commercial landscape that defines Vancouver Island, shedding light on key trends, emerging opportunities, and the evolving dynamics that shape this ever-changing landscape.

Kevin Johnston, President of Strand, shares his expert perspectives on the market's current landscape and interest rates, and unpacks the opportunities and challenges that shape Vancouver's real estate scene. We also dive into the office asset class, which seems to be bubbling under the surface with potential.

Meg Cooney, Commercial Real Estate Broker at WWC Vancouver, dives deep into a transformational approach that draws people back to offices without enduring long commutes. This isn't just a discussion about office spaces—it's a blueprint for redefining the future of our communities.

Cory Wright, Founder of William Wright Commercial, avid real estate investor, and—most importantly—one of the best dealfinders we’ve ever met, holds a master class on how to choose residential and commercial real estate markets, find and analyze the best deals, and implement advanced strategies to supercharge your portfolio.

Gordon MacPherson, President of Elevate Development Corp, provides expert insight into the current real estate market and its dynamic nature. We talk about how different asset classes have been affected since the pandemic, and gain valuable knowledge on the evolving trends in walkable village concepts within various areas.

With his finger on the pulse of international markets, Peter Leung, investorpreneur and international correspondent for the show, offers unique insights that can give you a competitive edge. Discover his surprising choices on whether to buy or sell, and prepare to be astounded by his current preferred investment hotspot.

Jon Switzer, Managing Partner and Commercial Mortgage Broker at Impact Commercial, sheds light on the recent interest rate adjustments and their impact on individuals and businesses alike. Gain a deeper understanding of how these changes reverberate throughout the market and explore the potential ramifications for the local economy.

Shawn Bouchard, Chief Operating Officer of Lorval Developments, dives into the pressing issue of Vancouver's rental housing crisis, unpacking his thoughts on the root causes of the problem and offering valuable insight on potential solutions. Discover how government intervention can play a pivotal role in addressing the challenges faced by renters in Vancouver.

Lori Suba, President and Broker, and Laurae Spindler, Vice President and Associate, of Scout Real Estate revisit the market in Calgary. Lori and Laurae unpacks the different sectors of the market, as well as discusses the Calgary downtown core and shares what the future could entail for Canada’s top 2023 market.

Marianne DeCotiis, commercial real estate broker at William Wright Commercial Kamloops, digs into the Kamloops market. How has the commercial market changed and developed over the past few years? What is the current state of supply? How have the operations of the commercial market shifted?

Bronwyn Scrivens of Omada Commercial unpacks Alberta market lease rates, the differences between Calgary and Edmonton when it comes to being an industrial landlord, how prices have changed, and where she would invest if she were to walk into the market today.

William Wright Commercial's very own Rod MacKay is here to give us a general update on the market. How have interest rates affected the market? How is the supply? What is the vacancy rate doing? And how is the retail market fairing after the pandemic?

Paul Sullivan, property tax expert from Ryan ULC, unpacks some potentially business saving insight as he guides us through the labyrinth of commercial property tax. What are commercial tax classes? Which areas are taxed the most and how do they work it out?

Retail expert David Ian Gray of DIG360 unwraps everything from how the retail environment has changed, why American big box brands haven't fared as well this side of the border, how technology has impacted the retail world, and his thoughts on why Nordstrom is pulling out.

Ever wonder how companies buy commercial buildings, fix them up, keep them, and then seem to buy more? Cory and Melisa walk through the 5 key indicators and steps on how you can buy value-add properties and get a 100% return on your equity in under 2 years.

As interest rates continue to move upward, how can you cash in on this? Lawrence Green, President of Spire Development Corporation, discusses what he sees happening in BC’s best markets and how you can make money from these high interest rates.

Why is the collapse of Silicon Valley Bank good for real estate in BC? Alan Haigh, Founding Partner of Impact Commercial Group, discusses how the shocking events down south with SVB could impact BC real estate. Alan shares how rates may move sooner than expected or how they may hold firm for 2023.

From securing air right for a crane to ensuring the land doesn't give way for your underground parkade, Tim Sportschuetz of Sportschuetz & Co construction lawyers talks about all the things you would have never guessed that go into a real estate development in BC.

What’s the last BC commercial real estate market left to boom? Kevin Wong of Wesbild discusses everything Kamloops and why this market is about to boom, from major industries driving the local economy to AAA tenants looking to enter the market.

Conall Barr of CBarr Inspections discusses the importance of a commercial building inspection before you remove subjects on your next purchase and how it can save a buyer hundreds of thousands of dollars in deferred maintenance costs.

Why did we pick Nanaimo as the best investment market for 2023? Connor Braid of William Wright Commercial and Managing Director for Vancouver Island shares the inside stats on why the Central Island region is an investment market you want to know.

Thomas Wieckowski, Associate Appraiser of Campbell & Pound, discusses what’s in store for 2023 and a lookback at the past 24 months. Thomas walks us through what the appraisal industry has seen over the past 2+ years and gives his thoughts on what makes a good opportunity.

Who better to hear from on how 2023 is shaping up than an appraiser who sees all the deals and numbers? Commercial appraiser Ryan Wong from Ryan LLC lets us in on what he is seeing. Will the market collapse in 2023? Will inflation topple the market? Will we see gains in real estate assets in BC this year?

Ever wonder what it would be like to be part of a $1,000,000,000+ portfolio of real estate? Alex Messina, VP of Acquisitions for Nicola Wealth Real Estate, which oversees over $8.5 billion dollars worth of some of the best real estate in North America, shares their strategy and where they are most excited about for 2023.

With the Bank of Canada’s latest rate increase of 0.25% and what could be the last rate increase for 2023, what does this all mean? BMO's Chief Economist Doug Porter shares his thoughts on interest rates, inflation, the overall Canadian economy, our neighbours to the south, and everything else you need to know for 2023.

Phones are already ringing for properties and sellers are receiving offers—in some cases multiple... So what does it all mean? Patrick Wood from WWC’s Victoria office tells us how to interpret this quick start to 2023, what his picks are for best investment markets, and what he anticipates all these numbers reveal about interest rates and inflation.

Rod MacKay from William Wright Commercial shares the 5 best commercial investment markets for 2023. These markets offer above average returns with the opportunity for a major increase in net operating income in the coming years, resulting in a big potential equity gain.

As 2023 is now in full swing and the real estate markets are off to a rocky start, Alan Haigh of Impact Commercial sheds some light on where interest rates are going, when they might pull back, and how to take advantage of this market turbulence to find a deal.

Happy Holidays, Happy Hanukkah and Merry Christmas from all of us at the VCREP and thanks for listening in 2022. As the podcast continues to grow week-over-week we have some amazing guests lined up for 2023 which is shaping up to be our biggest year yet. Thanks for all the continued support and we look forward to some amazing shows in 2023!

Jon Switzer of Impact Commercial shares that the 10-year bond numbers were falling, which predicts (fingers crossed) that fixed rates will follow. Jon shares his prediction on interest rates for 2023 and when he sees rates pulling off and declining. If you have a mortgage, this is an episode you must take in.

Everyone's always looking for the next asset class to buy, and we know what it is for 2023. Adam Mitchell of Low Tide Properties discusses Lab 29 and what could be the most sought-after asset in Vancouver: industrial lab space. He also shares why Low Tide continues to invest in this sub-asset class and why it's in such high demand.

Daniel Eagling from Cairn Homes in Ireland discusses how inflation, interest rates, and supply chains are affecting their market. Dan walks us through the challenges their market and the neighbouring European markets are having, the strain on supplies, and the tightening of the rental market heading into 2023.

William Wright Commercial operates offices in five of BC’s top commercial real estate markets, and with two more offices set to open in the coming months, who better to get a province-wide view on the markets than WWC’s Business Development Manager, Matt Everitt? Matt discusses why the time is now for investors to jump into these areas.

As people trickle back to the office in one fashion or another, is an investment into an office space the best opportunity in 2023? Byron Chard, CEO and President of Chard Development, discusses his latest office projects, along with the success of those projects and everything Chard has on the books for 2023 and beyond.

Brad Howard, Director of Development at PCI Developments, discusses the Lower Mainland's second downtown in Surrey and talks about PCI Developments' exciting and recently completed project, the King George Hub. Brad unpacks the success of the project, why it is desperately needed in Surrey, and the rapidly growing downtown district in Surrey Central.

Do you own land in BC? Are you required to file under the Land Owner Transparency Act by November 30th? Commercial real estate legal expert Scott McInnes of Redpoint Law discusses this all-important deadline for BC landowners, unpacking what exactly the Land Owner Transparency Act is, if it applies to your property, and more importantly, if you are required to file by November 30th, 2022.

How are the current economic challenges affecting the development industry? Jordan MacDonald, CEO of fabric living, opens up about the challenges the industry has faced with rising inflation and interest rates, how fabric has navigated the current economy, and how he and his team have continued to grow and acquire assets during this time.

Did you know that business sales and acquisitions fall under the commercial real estate umbrella? Chris van Vliet from WWC's Fraser Valley office breaks down how you buy or sell a small business. He talks us through the timelines, the conditions, and some things you need to be cautious of when navigating through the process.

William Wright Kelowna's Team Leader Jeff Brown discusses whether or not Kelowna has felt any slow down like most markets have experienced. He also shares insight on what impact, if any, interest rates and inflation have had on the market, what asset classes continue to outperform, and what's next for Canada's fastest growing population.

Frank O'Brien shares Western Investor's top cities for commercial real estate in 2023. This year's list has a few VCREP favourites plus a couple surprises, not to mention the #1 spot isn't even in BC! Frank also shares his opinion on David Eby's new housing plan and how it could be opening an even bigger opportunity for speculators.

Impact Commercial's Co-founder and Managing Partner Alan Haigh unpacks what has happened over the past couple of months in both Canada and the US, how the bond market could predict what will happen to interest rates, and when this madness will end.

As the world continues to cope with rising inflation and interest rates, international commercial real estate investor Peter Leung tells us how his portfolio is (or isn’t) affected and what markets have bounced back quicker than others. Peter also discusses what BC markets he likes and where he is looking to grow his holdings.

As interest rates continue to push upwards, Harry Jones of William Wright Commercial Victoria discusses the Greater Victoria market that just doesn't slow down regardless of market conditions, and walks through all the asset classes and how they have performed over the past year and what is to come as interest rates continue to rise.

Ever wonder why or even how your property taxes go up every year? Clayton Olson of Altus Group discusses the metrics behind your commercial property taxes. He walks through how these costs are calculated, why they increase, and what you can do if you disagree with your tax amount.

How can you benefit from a life insurance policy while you're still alive? Robert Trasolini and Laurent Munier of Safe Pacific Financial show just how easy it can be to use a life insurance policy as an investment vehicle to drive you into the commercial real estate game.

Why are my premiums going up so fast on my real estate insurance? Nigel Clark of BFL Canada, one of the largest risk management, insurance brokerage and benefits consulting firms in Canada, talks about how inflation, interest rates, and rising construction costs all impact the insurance market.

Mayor Ed Mayne discusses the exciting opportunities Parksville is currently experiencing in the Central Island market. As Nanaimo continues to boom, just 20 minutes up the road sits Parksville, which has seen a development boom of their own, led by a proactive mayor who has the experience to guide the community into 2022 and beyond.

If you were shocked by the Bank of Canada's 1% increase to interest rates this past week, you're not alone. Cory and Matt discuss the potential impact on commercial real estate... if any all. How does this affect your loan-to-value ratio when looking to acquire real estate? And what's next for the commercial real estate market in the province?

Which commercial market has the whole country talking? Lori Suba and Laurae Spindler of Scout Real Estate in Calgary unpacks the rollercoaster of action the Prairies are experiencing in the commercial market. You might be surprised to hear there's now overwhelming demand for one asset class in particular, which has seen growth in numbers similar to that of BC!

Jeff Kennedy of Troika Developments, one of Kelowna's most well-known builders, discusses the challenges in the development industry due to supply chain issues and inflation. He also gives insight into how developers would break down a purpose-built rental project vs. a strata site, along with the metrics behind the decision-making process.

For 24 months and counting, Vancouver Island has become a shining star in the commercial real estate world. John MacDonald, publisher of the Business Examiner, one of Vancouver Island's go to online business publications, unpack the numbers, breaks down how the Island markets fared, and provides insight on the Thompson Okanagan region.

Hear from the man who plausibly has more data on commercial real estate than anyone in Canada. Raymond Wong, VP of Data Operations at Altus Group, looks behind the numbers on what has happened across Canada in 2022 and unpacks which asset classes are selling, which are not, and what is set to rebound.

With the new Broadway Skytrain line in full swing, city council members now have to vote on what could be the biggest vote in Vancouver's history. Meg Cooney, Seamus Bailey, and Liam Simpson of WWC discuss the highlights and lowlights of the proposed plan.

The ongoing debate on Vancouver Island right now is Victoria or Nanaimo? Robin Kelley of the Groupe Denux, one of Vancouver Island’s long-standing families of real estate, provides insight on both markets and how each market has fared over the years, and unpacks which asset classes he thinks will continue to grow.

Rod MacKay of WWC’s Vancouver office discusses the most unpredictable year we’ve had in real estate yet. From faster than expected rising interest rates, to record breaking month-over-month inflation, to worldwide supply chain issues… 2022 has been anything but predictable.

Ever find a great restaurant on your favourite food app, but then realize they don’t have a brick and mortar location you can enjoy? Amrit Maharaj, Chief Operating Officer of Coho Collective, breaks down what a ghost kitchen is, why restaurants are getting in on the action, and how they have capitalized on the food app boom.

Bronwyn Scrivens from Omada Commercial Real Estate in Edmonton discusses Alberta’s growing industrial market. She shares how Alberta is receiving the halo effect from BC’s tight vacancy rates and staggering acquisition costs, and what tenants and developers are now looking into when it comes to Alberta vs BC.

One of the biggest secrets in commercial real estate is spotting the trends and staying ahead of them. Jonathan Meads, Vice President of StreetSide Developments, discusses the booming Fraser Valley markets and unpacks why StreetSide keeps their focus primarily on this area.

On a national and provincial level, one of the most exciting real estate markets has been Victoria. Mayor of Victoria, Lisa Helps, unpacks how Victoria got to where it is today, the goals she has accomplished in her eight years as mayor, and unveils what’s in store for BC’s capital city.

If you’ve been following the real estate markets in BC, you’ll know today’s hottest topic is the rapidly rising interest rates. Jon Switzer of Impact Commercial sheds light on how to navigate the next few months and provides tips on what to look for in your next purchase to maximize your lending ability.

Mike Kozakowski, founder of Citified Media and citified.ca, a comprehensive resource for researching new-build homes and commercial spaces on Vancouver Island, gives a glimpse into the years and years of new construction data Citified has tracked in the Greater Victoria area.

Sam Wilson, renowned host of the hugely popular podcast, How to Scale Commercial Real Estate, uncovers his roots in commercial investing, shares some mistakes he has made along the way, and talks us through what a good deal looks like to him.

If you had to guess which real estate market saw one of the biggest increases in commercial property value over the past 2 years, would you have guessed Chilliwack? David Algra of Algra Bros. Developments discusses their current downtown Chilliwack project, District 1881.

Leonard Krog, Mayor of Nanaimo, shares some great insight on all the new and upcoming projects and what the future holds for the port city. Plus, we dive into the highly anticipated and forthcoming OCP for the downtown and surrounding areas.

Cory and the team are hitting the beach this week for a well deserved break. Next week we are back with another phenomenal episode. Stay tuned!

Named Canada’s fastest growing city with a 14% increase in population since 2016, Jon Friesen, CEO of the Mission Group, the company behind some of Kelowna’s spectacular tower developments, discusses why Kelowna has seen such a massive growth over the past 5 years and what the future looks like.

Recently named BC’s most resilient economy by BC Business Magazine, Langford could be BC’s next big thing. Mayor Stewart Young discusses the amazing developments happening throughout the city and story of how Langford landed Costco, followed by Home Depot, and now Tesla Motors.

Ever wonder if you could buy an office building or a retail shopping mall for only $150,000? Darcy Ulmer, Co-founder and Partner at Stream Property Partners, shares how everyday investors can invest in some big commercial real estate assets for a fraction of the purchase price.

Have you ever wanted to make the money real estate developers do? Ravi Mann of PROPetual REIT and the Isle of Mann Property Group discusses the exciting new investment opportunities that can get anyone through the real estate investment door for as little as $5,000.

Have you ever wanted to make the money real estate developers do? Ravi Mann of PROPetual REIT and the Isle of Mann Property Group discusses the exciting new investment opportunities that can get anyone through the real estate investment door for as little as $5,000.

As Canada and the world continues to battle with Omicron, supply chains are challenged and the Bank of Canada surprisingly holds rates. Doug Porter, Chief Economist & Managing Director of BMO Financial Group, shares his thoughts on what’s next for the economy and his prediction for interest rates.

Ever wonder which commercial asset class has the lowest cap rate but offers the most stable returns? Marianne DeCotiis, a multifamily specialist with WWC, breaks down the multifamily asset class, sharing how it’s funded, how the leases are government regulated, and plenty more!

Over the past 20 months, most industries have seen a lot of change and the law industry is no different. Tim Lack of Redpoint Law discusses the ever-changing world of the legal side of commercial real estate and shares insight on how the pandemic has changed how commercial real estate is leased, sold, and financed.

Over the past 20+ months, we have heard about supply chain issues, labour shortages, and logistical challenges, and this all has a direct impact on the construction of real estate in the province. Owen Lecky of Wales McLelland unwraps the issues that have been affecting our real estate market.

Do you own a property with lots of equity that has built up over the years? Alan Haigh of Impact Commercial Group, one of BC’s leaders in commercial mortgages, explains how to tap into that equity and turn one property into a thriving commercial portfolio without having to sell your asset.

Wishing our listeners a Merry Christmas and a Happy New Year!

For all the curious minds interested in commercial real estate investing, grab a coffee and pull up a chair because we have exclusive stories and tips from commercial real estate brokers, investors, developers, economists, urban planners, and everyone in-between. From the successes and failures to the motivations and lessons learned, the Vancouver Commercial Real Estate Podcast is your insight into commercial real estate in Vancouver, Victoria, Kelowna, and beyond.

What's the best real estate market to invest in? What are the commercial real estate asset classes and property types? Hosted by Cory Wright, founder of William Wright Commercial, and co-hosts Adam and Matt Scalena of the Vancouver Real Estate Podcast, our podcast opens the door to real estate investing for everyone from beginner investors to experienced real estate professionals. New episodes are released every Tuesday. Follow the Vancouver Commercial Real Estate Podcast on Apple Podcasts, Spotify, Google Podcasts, or your favourite streaming platforms.

Sign up to the William Wright Commercial newsletter for commercial real estate listings, news and more.

SubscribeThis communication is not intended to cause or induce breach of an existing agency agreement. E&OE: All information contained herein is from sources deemed reliable, and have no reason to doubt its accuracy; however, no guarantee or responsibility is assumed thereof, and it shall not form any part of future contracts. Properties are submitted subject to errors and omissions and all information should be carefully verified. All measurements quoted herein are approximate.

ⓒ William Wright Commercial Real Estate Services 2024

Proudly designed by Burst Creative